Comparing debt relief options? Relief helps eligible users request lower balances with one flat monthly membership rather than a multi-year plan that repays your full balance at a lower interest rate, the way an InCharge debt management plan works. Keep more of your savings and get tools designed to help reduce collection calls along the way.

One flat monthly membership · No percentage cut of your settlements · Cease & desist letters included

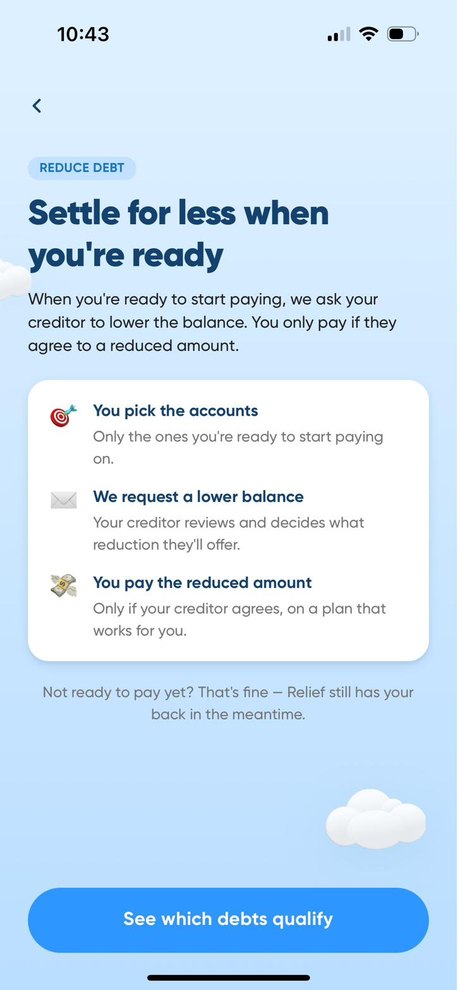

InCharge Debt Solutions is a nonprofit credit counseling agency, not a settlement company — its debt management plan rolls your credit-card debt into one monthly payment at a lower interest rate, but you repay the full balance. Relief takes a different starting point: it’s not just about settling — it’s an app for people in collections that silences harassing calls with cease & desist letters, monitors every contact for FDCPA violations, and lets you settle when you’re ready, all under one flat monthly membership. The whole settlement process is automated through the app, and you’ll see the typical reduction percentage for each creditor before you approve anything.

Inside the app

Side by side

An app that settles your debts for less — for one flat monthly membership — and silences harassing calls and catches FDCPA violations along the way.

A debt management plan: one monthly payment to InCharge, distributed to your creditors at a lower interest rate.

People who want to settle their debts for less without handing over a big percentage — and want the collection calls to stop, too.

People who can afford to repay the full balance and want a structured plan with lower interest, not reduced principal.

One flat monthly membership. No per-letter fees, no per-request fees, and no percentage cut of your settlements.

A setup fee (around $50) and a monthly fee (around $30) — not a percentage of your debt. You repay the full balance you owe.

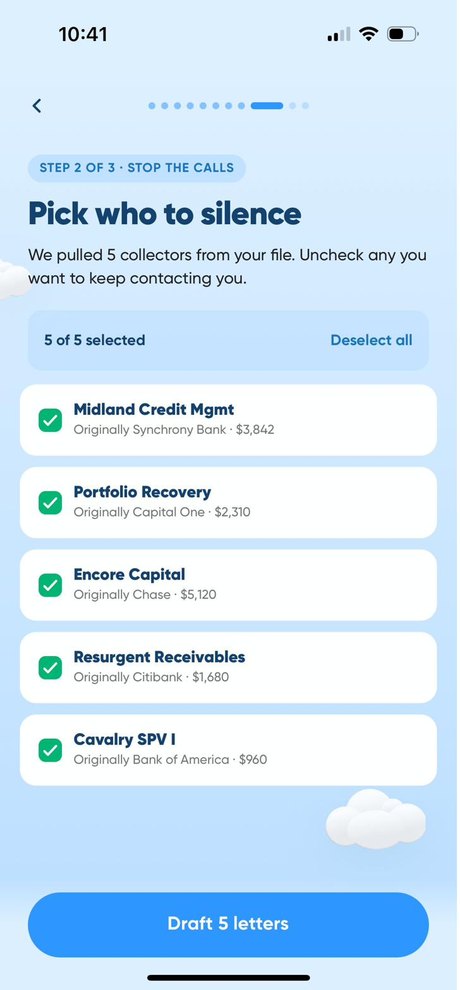

Cease & desist letters are drafted and delivered for you — calls typically quiet down within 30–60 days.

Accounts on the plan get paid monthly, so calls on those ease — but a DMP doesn’t send cease & desist letters.

Every collector contact is logged and monitored for FDCPA violations. A documented violation can mean up to $1,500 in some cases — or leverage toward a full settlement of the account.

Not part of a debt management plan.

Three options in-app: an AI-drafted response (included), a lawyer-drafted response (flat fee), or hiring an attorney end-to-end at a discounted rate. Court filing fees may apply.

A debt management plan doesn’t handle lawsuits. Accounts left off the plan, or missed payments, can still lead to court.

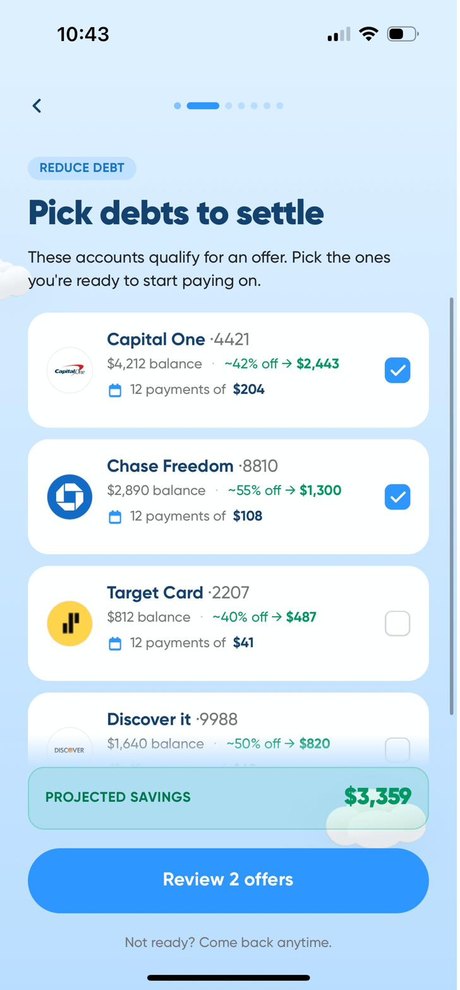

When you’re ready, the app automatically requests settlement offers from your creditors and shows the typical reduction for each one before you decide.

Not offered. A DMP lowers your interest rate and repays the full balance — it doesn’t reduce what you owe.

You’re a member from day one, and cease & desist letters can go out right away. Settlement requests are sent automatically; if a creditor agrees and you approve, you pay your creditor directly.**

Free initial counseling, with no credit score or minimum balance to enroll; you close your credit cards and repay over three to five years (36–60 months).

The big difference

On an InCharge plan you repay the full balance you owe, just at a lower interest rate, plus a setup fee (around $50) and a monthly fee (around $30). Relief is one flat monthly membership and helps you settle for less than the full balance — with no percentage skimmed off your settlements.

For most balances, that makes Relief the more affordable way to settle for less.

Why people pick Relief over InCharge Debt Solutions

A debt management plan isn’t built to stop collector contact, and it doesn’t cover accounts already in collections. Relief drafts and delivers real cease & desist letters for you, and the calls typically quiet down within 30–60 days. Every contact is logged and checked for FDCPA violations, worth up to $1,500 each in some cases.

A debt management plan doesn’t make you lawsuit-proof; accounts left off the plan can still go to court. Relief builds the response into the app: an AI-drafted response included with membership, a lawyer-drafted response for a flat fee, or hiring an attorney end-to-end at a discounted rate. Court filing fees may apply.

Automated through the app

Illustrative reductions. Actual offers vary by creditor and account — you see each one in the app before you decide.

Common questions

Settle your debts for less, keep more of the savings, and get the calls to stop — all from your phone, all in one flat monthly membership.

Get the app**After a settlement request is sent, creditors have 60 days to respond. If a settlement is reached and you approve it, you pay your creditor directly.

Relief is not a law firm and does not provide legal advice. Relief members receive cease & desist letters, collector-violation monitoring, and access to legal services through independent attorneys for certain matters. The attorney-client relationship, if any, is between the member and the independent attorney for the specific matter.

Comparison figures for InCharge Debt Solutions reflect publicly reported program terms (industry reviews and CFPB guidance) and vary by state and individual circumstances. Current as of June 2026.

Relief is not affiliated with, endorsed by, or sponsored by InCharge Debt Solutions. InCharge Debt Solutions and its logo are trademarks of their respective owners and are used here for comparison and identification only.

About Relief: Relief is a self-service platform designed to help you understand and take action on your debt. We are not a lender, creditor, debt collector, or law firm.

How It Works: Relief provides tools to help you review your accounts, understand your situation, and explore potential options available to you. Depending on your eligibility, you may be able to take action directly through the platform, including submitting requests to your creditors or choosing to contact your creditor directly. Creditors independently review any requests and determine whether to accept, reject, or provide alternative terms. Results vary based on your situation and each creditor’s policies. There is no guarantee of any specific outcome.

Fees & Payments: Relief charges a membership fee for access to its platform and tools. These fees are for use of the platform only and do not go toward payments to your creditors. If a request is accepted, your creditor will provide payment terms directly. You are responsible for making all payments according to those terms.

Membership Includes: With your membership, you have access to a growing suite of tools designed to help you better understand, manage, and take action on your debt. This includes access to data-driven insights and technology that analyze your accounts and surface potential options, along with tools to review important notices, identify opportunities, and take next steps directly through the platform. Available tools and features may change or expand over time.

Account Information: Account details, balances, and eligibility are based on the most recent data from your credit report and may change over time. We cannot edit, modify, add accounts or details shown from these reports.

Legal Information: Legal Protect tools are provided for informational purposes only and do not constitute legal advice or legal representation.

Reduction Tool: Our reduction tool uses first-party and third-party data to estimate what creditors may be willing to accept for less than the full balance. These are estimates only, and all reduction terms and outcomes are determined solely by your creditor. Users with eligible debt may request to receive an offer to resolve an account for less than the full balance. Outcomes vary, and there is no guarantee of reduction. Creditor responses may take up to 60 days. If an offer is available, your creditor will provide the final terms, including any repayment schedule. You pay your creditor directly. Relief does not collect or process payments on behalf of creditors.